Why Do Mortgage Applications Get Rejected?

Applying for a home loan is a monumental step toward property ownership, but for many, the journey hits a roadblock when they receive a rejection letter from the bank. Understanding why mortgage applications get rejected is essential for any prospective homebuyer looking to navigate the complex world of finance. Whether you are a first-time buyer or looking to refinance, identifying the reasons for mortgage denial can help you pivot from a rejection to an approval.

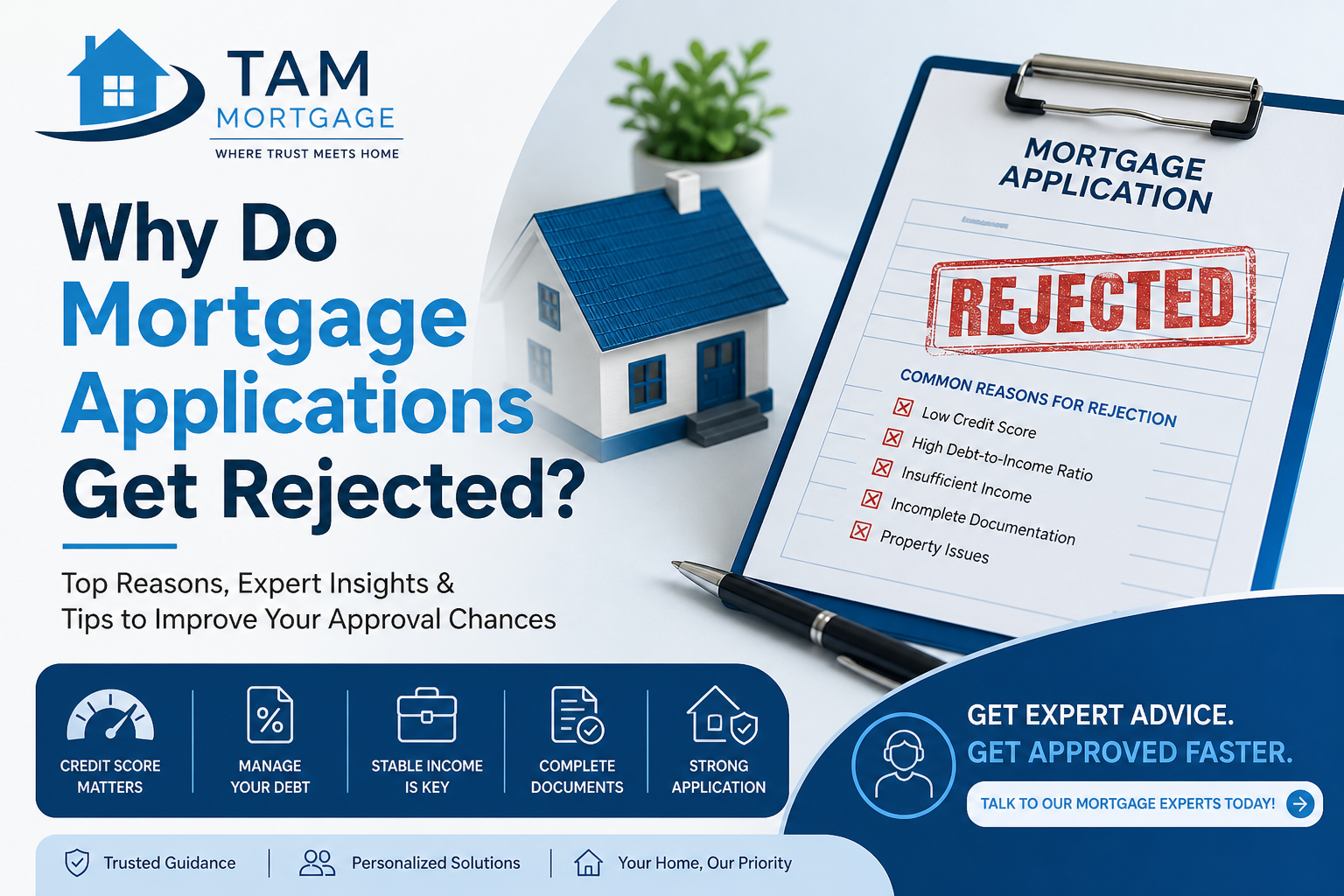

Quick Answer: Top Reasons for Mortgage Rejection

A mortgage application is typically rejected due to a few primary factors: a low credit score, a high debt-to-income (DTI) ratio, unstable employment history, or discrepancies in documentation. In many cases, banks also reject loans if the property itself has legal or title issues. By addressing these core areas, you can significantly improve your loan eligibility.

Top Reasons Mortgage Applications Get Rejected

The bank’s underwriting process is designed to assess your repayment capacity and overall financial stability. If any part of your profile suggests high risk, the application may be declined.

1. Low Credit Score

Your credit score is often the first thing a lender looks at. It reflects your credit history and how reliably you have managed past debts.

- The Impact: A low score suggests a history of late payments or defaults, making lenders hesitant to offer large sums of money.

- The Goal: Most lenders prefer an ideal credit score of 750 or above to ensure the best interest rates and approval chances.

2. High Debt-to-Income (DTI) Ratio

Lenders use the DTI ratio to determine if you can afford another monthly payment.

- The Formula: This is calculated by dividing your total monthly debt obligations by your gross monthly income.

- The Threshold: To maintain high loan approval factors, you should aim to keep your DTI under 40%. If your existing loans (car, personal, or credit cards) consume too much of your paycheck, the bank will likely reject your mortgage application.

3. Unstable Employment or Income

Banks seek certainty that you will have a steady stream of income for the next 15 to 30 years.

- Salaried vs. Freelancers: While salaried employees are often viewed as lower risk, freelancers or self-employed individuals may face more scrutiny regarding their income verification.

- Stability Requirement: Lenders typically look for a stable job history of at least 6 to 12 months with the same employer or in the same industry.

4. Incomplete or Incorrect Documentation

The bank underwriting process is rigorous and requires a mountain of paperwork.

- Common Errors: Missing KYC documents, mismatched signatures, or incomplete bank statements can lead to an immediate rejection.

- Accuracy Matters: Ensuring all documentation is correct and up to date is one of the easiest ways to prevent unnecessary delays or denials.

5. Property Issues

Sometimes the rejection has nothing to do with your finances and everything to do with the home you want to buy.

- Legal & Title Problems: If the property has legal disputes, unclear title deeds, or does not meet the bank’s internal safety standards, the loan will be denied.

- Valuation Gap: If the bank’s appraisal is significantly lower than the purchase price, they may refuse to fund the requested amount.

6. Too Many Recent Loan Applications

Every time you apply for a loan, the lender performs a “hard enquiry” on your credit report.

- Credit Impact: Too many enquiries in a short period signal “credit hunger” or financial distress, which can lower your score and lead to home loan rejection causes.

Real-Life Example: Rahul’s Rejection

Consider the case of Rahul, a prospective buyer who recently applied for a home loan. Rahul had a high-paying job and a decent credit score, yet his application was rejected. Upon closer inspection, it was discovered that Rahul had recently taken out a car loan and had several active credit card EMIs, pushing his Debt-to-Income ratio well above 50%. Because he failed to manage his existing debt before applying for a mortgage, the bank viewed him as a high-risk borrower. By paying off his smaller debts first, Rahul was eventually able to reapply and secure approval.

What To Do If Your Mortgage Is Rejected?

Receiving a denial doesn’t mean you will never own a home. It simply means you need to adjust your strategy.

- Identify the Root Cause: Ask the lender for a specific reason for the rejection.

- Improve Your Credit Profile: Focus on paying down existing debts and ensuring no payments are missed for several months.

- Correct Document Errors: Double-check your KYC and financial statements for any inconsistencies.

- Wait Before Reapplying: Don’t rush to another bank immediately, as multiple rejections can further damage your credit score.

- Choose the Right Lender: Some banks have stricter mortgage approval criteria than others; research which lender best fits your specific financial profile.

How to Avoid Mortgage Rejection? (Pro Tips)

Prevention is better than cure. Follow these expert tips to ensure your application is “bank-ready” from day one:

- Maintain a Credit Score Above 750: This is the gold standard for easy approval.

- Keep DTI Under 40%: Ensure your existing monthly debts are manageable.

- Stable Job History: Remain with your current employer for at least 6–12 months before applying.

- Avoid Large Transactions: Do not make any last-minute large purchases (like a new car or expensive furniture on EMI) right before or during your mortgage application process.

Mortgage Rejection Checklist

Use this checklist to verify your readiness before you hit “submit”:

- [ ] Credit score checked and verified above 750.

- Income proof ready (Pay slips, ITR, and bank statements).

- Debt under control (DTI ratio calculated and minimized).

- Property verified (Title deeds and legal documents reviewed).

Can You Reapply After Rejection?

Yes, you can reapply, but timing is everything. You should generally wait until you have significantly improved your financial profile. Reapplying immediately with the same profile will likely result in another rejection and further harm your credit score.

When Should You Consult a Mortgage Expert?

Consulting an expert is highly recommended if you have a complex income structure (such as being self-employed), have faced a previous rejection, or are a first-time buyer confused by the process. Speaking to an advisor can help you navigate the bank underwriting process and find the best path to approval.

FAQs

Does a mortgage rejection affect my credit score?

The rejection itself doesn't show on your score, but the hard enquiries made by the bank during the application process can lower it.

How long should I wait after a rejection to reapply?

It is usually best to wait 3 to 6 months while you work on improving your credit score and reducing debt.

What is the minimum credit score required?

While some lenders accept lower, a score of 750+ is generally required for smooth approval.

Can self-employed people get approved?

Yes, but they must provide extensive income verification and tax returns to prove financial stability.