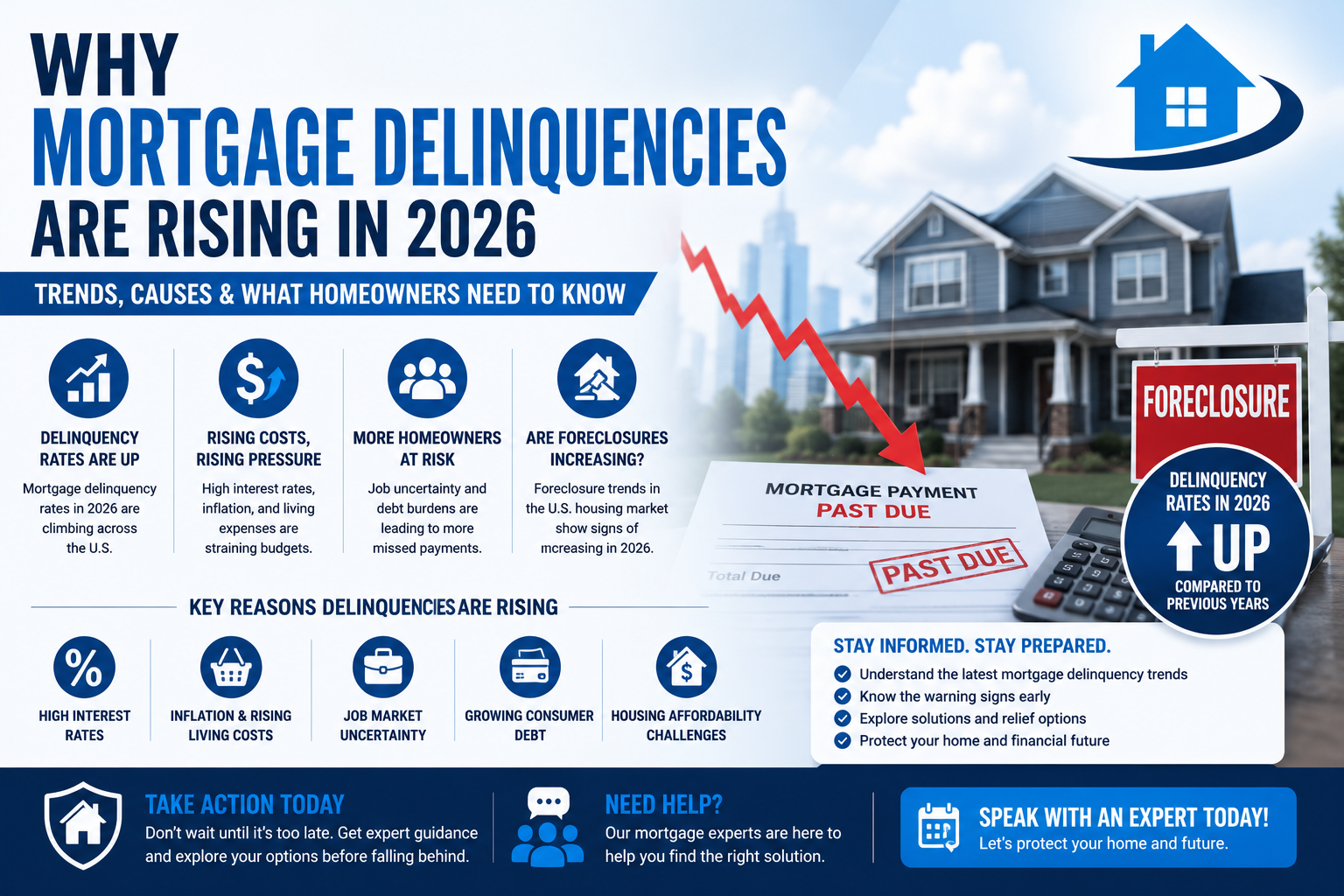

Why Mortgage Delinquencies Are Rising in 2026? Foreclosure Trends & Housing Market Risks

A growing number of American homeowners are struggling to keep up with their mortgage payments, and the numbers are becoming increasingly difficult to ignore. After years of low interest rates and pandemic-era financial support, many households are now facing rising costs, financial pressure, and economic uncertainty. As mortgage delinquency rates continue to climb, understanding the reasons behind this trend has become more important than ever for homeowners, buyers, and investors alike.

What Is Mortgage Delinquency?

Definition of Mortgage Delinquency

Mortgage delinquency occurs when a borrower misses one or more scheduled mortgage payments. Even a single missed payment can negatively impact a borrower’s credit score and trigger lender communication regarding overdue balances.

Stages of Delinquency

Mortgage delinquency typically progresses through stages. A payment that is 30 days late serves as the first warning sign. At 60 days past due, lenders usually intensify collection efforts. Once payments are more than 90 days overdue, the loan enters serious delinquency status, increasing the likelihood of foreclosure proceedings.

Difference Between Delinquency and Foreclosure

Delinquency refers to missed payments and acts as an early warning stage, while foreclosure is the legal process through which a lender attempts to recover the property after prolonged non-payment. Acting early during delinquency can help borrowers avoid foreclosure altogether.

Mortgage Delinquency Trends in 2026

Current Mortgage Delinquency Rates in 2026

Mortgage delinquency rates have steadily increased across the United States. Data from recent reports indicates higher stress among borrowers, especially those with FHA loans and adjustable-rate mortgages. Rising foreclosure inventories also suggest that more homeowners are struggling to remain current on their payments.

Which States and Cities Are Most Affected?

Certain regions are experiencing sharper increases in mortgage delinquencies than others. Lower-income areas and regions with rising unemployment are seeing the highest levels of financial strain, while wealthier communities remain relatively stable.

Comparing 2026 Delinquency Rates to Previous Years

Although delinquency rates are rising, they remain significantly lower than the levels seen during the 2008 financial crisis. Experts suggest the current situation reflects growing financial stress rather than a full-scale housing market collapse.

Why Are Mortgage Delinquencies Rising?

High Interest Rates and Mortgage Costs

Borrowers with adjustable-rate mortgages are experiencing higher monthly payments as interest rates continue to rise. Refinancing options have also become less attractive due to elevated mortgage rates.

Inflation and Rising Living Expenses

Persistent inflation has increased the cost of everyday essentials such as food, fuel, utilities, and insurance. As living expenses grow, many households are finding it more difficult to keep up with mortgage obligations.

Job Market Uncertainty

Changes in the labor market and rising unemployment in certain regions are affecting borrowers’ ability to manage debt. Income instability has become a major contributor to missed mortgage payments.

Growing Consumer Debt

Americans are carrying record levels of credit card debt, auto loans, and personal loans. When combined with rising mortgage payments, these financial obligations can quickly become overwhelming for many households.

Housing Affordability Challenges

Many homebuyers stretched their finances during the housing boom of 2022 and 2023. With affordability already strained, even small increases in expenses or reductions in income can create serious financial difficulties.

Are Foreclosures Increasing in 2026?

Foreclosure Trends in the US Housing Market

Foreclosure activity is rising alongside delinquency rates. More homeowners are entering the foreclosure process as lenders respond to prolonged missed payments and increasing financial distress.

Why More Homeowners Are at Risk

Pandemic-era savings have largely been depleted, while higher mortgage payments and inflation continue to pressure household budgets. Many borrowers no longer have the financial cushion they once relied upon.

Which Borrowers Are Most Vulnerable?

First-time homebuyers, FHA borrowers, and homeowners with adjustable-rate mortgages are among the groups facing the highest risk of delinquency and foreclosure in 2026.

Economic Factors Affecting Mortgage Payments

Federal Reserve Interest Rate Policies

The Federal Reserve’s interest rate hikes have significantly increased borrowing costs. Although rates have stabilized somewhat, they remain much higher than the historic lows seen during the pandemic years.

Wage Growth vs Inflation

While wages have increased in some sectors, inflation has outpaced income growth for many households. This means mortgage payments now consume a larger portion of monthly earnings.

Property Tax and Insurance Increases

Homeownership costs extend beyond mortgage payments. Rising property taxes and increasing home insurance premiums are adding additional financial pressure on homeowners.

Rising Home Maintenance Costs

The cost of repairs, labor, and home maintenance remains elevated. Unexpected repair expenses can push financially stretched homeowners into delinquency.

How Mortgage Delinquencies Impact the Housing Market

Effects on Home Prices

Higher foreclosure rates can increase the supply of distressed properties, placing downward pressure on home values in certain markets.

Increased Housing Inventory

As more homes enter foreclosure pipelines, housing inventory may rise. While this could benefit buyers in some regions, it may also weaken local housing markets.

Impact on Lending Standards

Lenders are becoming more cautious by tightening lending requirements, increasing credit score expectations, and scrutinizing borrowers more closely.

Investor and Buyer Sentiment

Rising mortgage delinquencies often reduce confidence among homebuyers and investors, leading to slower market activity and more cautious purchasing decisions.

Warning Signs Homeowners Should Not Ignore

Missing Multiple Payments

Missing more than one mortgage payment is a clear warning sign that immediate financial action is needed.

Growing Credit Card Debt

Using credit cards to cover mortgage payments or everyday expenses can quickly worsen financial instability.

Using Savings for Basic Expenses

Relying on savings to pay for regular monthly bills indicates that household income may no longer be sufficient to cover essential costs.

Difficulty Managing Adjustable Mortgage Payments

Borrowers struggling with rising adjustable-rate mortgage payments should contact lenders early to explore available solutions.

What Homeowners Can Do to Avoid Foreclosure

Contact the Lender Early

Early communication with lenders can open the door to repayment assistance, loan modifications, or temporary payment relief options.

Request Loan Modification Options

Loan modifications can reduce monthly payments by adjusting interest rates, extending loan terms, or restructuring missed payments.

Explore Refinancing Solutions

Refinancing into a fixed-rate mortgage may help borrowers secure more stable and predictable monthly payments.

Consider Mortgage Forbearance Programs

Forbearance programs can temporarily pause or reduce mortgage payments for borrowers facing short-term financial hardship.

Work With Housing Counselors

HUD-approved housing counselors can help homeowners understand their options and negotiate with lenders when financial difficulties arise.

How Lenders Are Responding to Rising Delinquencies

Tighter Lending Standards

Banks and mortgage lenders are increasing underwriting standards to reduce future default risks and protect loan portfolios.

Increased Risk Assessment

Lenders are conducting more detailed financial evaluations and monitoring higher-risk borrower groups more closely.

Expanded Loss Mitigation Programs

Many lenders are expanding programs designed to help struggling homeowners avoid foreclosure through structured repayment plans and financial assistance.

Focus on Borrower Assistance

Financial institutions are increasing borrower outreach efforts to encourage early intervention before delinquency escalates further.

What Experts Predict for the Rest of 2026

Will Mortgage Delinquencies Continue Rising?

Experts expect mortgage delinquency rates to remain elevated throughout 2026, especially among financially vulnerable households and regions with economic instability.

Forecast for Foreclosure Activity

Foreclosure inventories are expected to continue increasing as more distressed borrowers enter the legal foreclosure process.

Housing Market Stability Outlook

Despite rising delinquencies, most analysts do not expect a repeat of the 2008 housing crash due to stronger lending standards and stricter underwriting practices.

Tips for Buyers and Homeowners in 2026

Buy Within Your Budget

Purchasing a home within a realistic budget can help reduce long-term financial stress and improve payment stability.

Build Emergency Savings

Maintaining emergency savings provides a financial buffer during unexpected hardships such as job loss or medical expenses.

Avoid Overleveraging

Borrowing conservatively helps homeowners remain financially flexible during periods of economic uncertainty.

Monitor Interest Rate Changes

Homeowners with adjustable-rate mortgages should closely track rate changes and prepare for future payment adjustments.

Improve Credit and Debt Management

Reducing debt and maintaining a strong credit score can improve financial stability and provide better refinancing opportunities.

Final Thoughts

Mortgage delinquencies are rising in 2026 due to a combination of higher interest rates, inflation, growing debt burdens, and economic uncertainty. While foreclosure activity is increasing, the current housing market remains more stable than during the 2008 financial crisis because of stricter lending practices and stronger borrower qualifications. However, homeowners must remain proactive, financially prepared, and willing to seek help early to avoid serious financial consequences.

FAQs

Does refinancing hurt your credit score?

Refinancing triggers a hard credit inquiry, which can lower your score by a few points temporarily. If you rate-shop multiple lenders within a 14–45 day window, most scoring models count all those inquiries as a single event.

How much equity do I need to refinance?

Most lenders require at least 20% equity for a standard refinance (80% LTV). For a cash-out refinance, most lenders limit the new loan to 80% of the home's value, though VA loans allow up to 100%.

Can I refinance with bad credit?

It's harder but not impossible. FHA streamline refinances and VA IRRRLs have more flexible requirements. A lower credit score will generally mean a higher interest rate, which may reduce the benefit of refinancing.

How soon can I refinance after buying a home?

For conventional loans, there's typically no mandatory waiting period, though many lenders prefer you've had the loan for at least 6 months. FHA and VA streamline refinances usually require a minimum of 6–12 months of on-time payments.

Can I refinance if I'm underwater (owe more than the home is worth)?

Standard refinancing requires equity. However, the High LTV Refinance Option (from Fannie Mae) and the Enhanced Relief Refinance (from Freddie Mac) may be available for underwater borrowers with on-time payment histories.